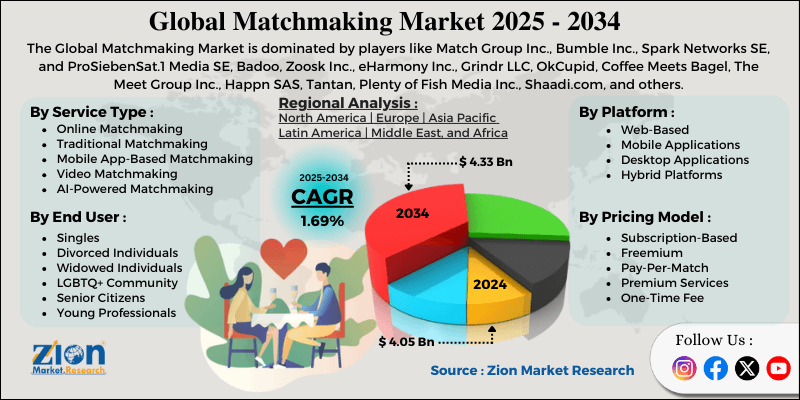

The matchmaking market, encompassing both online dating platforms and traditional services, continues to evolve rapidly in 2025, driven by technological advancements, shifting social norms, and a growing global population of singles. Valued at approximately USD 9.65 billion in 2025, the broader dating services industry including matchmaking is projected to reach USD 17.64 billion by 2033, growing at a compound annual growth rate (CAGR) of 7.83%. Within this, the core matchmaking segment alone is expected to hit USD 4.16 billion in 2025, with a more modest CAGR of 1.53% through 2029, reflecting a shift toward hybrid models blending AI personalization with human touch.

This analysis dissects the market into key segments: by service type, demographics (age, gender, and end-user), revenue models, geography, and emerging niches. Drawing from data sources like Zion Market Research, we highlight revenue breakdowns, growth drivers, challenges, and opportunities. Key insights include the dominance of mobile apps (over 80% market share), the rise of AI-driven personalization, and explosive growth in Asia-Pacific (CAGR of 13.48%). For businesses, the premium and niche segments offer high margins, while free-to-premium models drive user acquisition.

Whether you’re a platform operator, investor, or marketer, understanding these segments is crucial for capturing share in a market where 7.9% of global users now engage with dating services.

Introduction to the Matchmaking Market

Matchmaking has transcended its traditional roots think family introductions or speed-dating events to become a tech-infused ecosystem. In 2025, it includes algorithmic apps like Tinder and eHarmony, elite human-led services like Luma Luxury Matchmaking, and hybrid platforms integrating video calls and VR dates. The market’s expansion is fueled by rising smartphone penetration (over 6.8 billion users globally), declining stigma around online relationships (53% positive U.S. view), and post-pandemic loneliness affecting 1 in 3 adults.

However, challenges persist: user fatigue from swipe culture, privacy concerns, and market saturation in mature regions. Segmentation reveals untapped potential e.g., the 40+ age group growing at 9.9% CAGR in North America. This report uses bottom-up modeling from industry forecasts to provide actionable insights.

Market Segmentation Overview

The matchmaking market is multifaceted, segmented across multiple dimensions. Below, we break it down with 2025 revenue estimates, CAGRs to 2030/2033, and key trends. Data is aggregated from leading reports for a holistic view.

1. By Service Type: From Casual Swipes to Elite Introductions

Service types reflect user intent, from quick connections to committed partnerships. Online dominates, but offline and premium hybrids are rebounding.

| Segment | 2025 Revenue (USD Bn) | CAGR (2025-2030) | Key Trends & Drivers |

|---|---|---|---|

| Online Matchmaking (Apps & Platforms) | 7.92 (82% share) | 11.94% | AI algorithms (e.g., Tinder’s March 2025 AI tool); video-first features; 78% mobile app usage. |

| Offline/Traditional Matchmaking | 1.05 (11% share) | 6.7% | Cultural preferences in Asia; post-pandemic in-person events; personalized coaching. |

| Premium/Elite Services (Personalized Human-Led) | 0.68 (7% share) | 8.9% | High-net-worth clients ($5K–$250K packages); 48% YoY growth in luxury segment. |

- Insights: Online leads due to accessibility, but offline holds premium pricing power (ARPU up to $500/client). Niche hybrids like AI + human (e.g., Juleo’s LLM prompts) are bridging the gap, capturing 25% of new users.

2. By Demographics: Tailoring to Age, Gender, and End-Users

Demographics drive personalization. Younger users fuel volume; older cohorts boost revenue via subscriptions.

Age Group Breakdown

Younger segments dominate adoption, but seniors are the fastest-growing.

| Age Group | 2025 Market Share (%) | 2025 Revenue (USD Bn) | CAGR (2025-2030) | User Behavior |

|---|---|---|---|---|

| 18-25 Years (Gen Z) | 36% | 3.47 | 7.27% | Casual swipes; video chats; 42% use social discovery features. |

| 26-34 Years (Millennials) | 30% | 2.89 | 8.0% | Relationship-focused; high divorcee uptake; premium subs. |

| 35-50 Years | 20% | 1.93 | 9.9% | Work-life balance seekers; AI compatibility tools. |

| 50+ Years (Boomers/Seniors) | 14% | 1.35 | 4.81% | Companionship apps; security-focused; $4.6 Bn niche explosion. |

Gender and End-User Insights

- Gender: Females hold ~40% revenue share (USD 3.73 Bn in apps), growing at 4.81% CAGR due to safety features (e.g., Bumble’s verification). Males dominate volume (60%), but lower ARPU.

- End-Users:

- LGBTQ+ (38.67% share in niches; USD 3.72 Bn) – Grindr’s 25% Q1 2025 revenue jump.

- Divorced/Second Marriages (15% share) – Hidden $800 Mn India market.

- High-Net-Worth (7% overall) – $1.2 Bn premium; 62% prefer human matchmakers.

- Religious/Ethnic (e.g., Muslim/Hindu) – 12% share; fastest in India (11% CAGR).

- Insights: Gen Z’s aversion to swipes boosts “slow dating” (25% growth); Boomers seek ethics-focused platforms.

3. By Revenue Models: Subscriptions Fuel Stability

Monetization varies by user tolerance for payment.

| Model | 2025 Revenue (USD Bn) | CAGR (2025-2030) | Adoption Notes |

|---|---|---|---|

| Subscription | 5.20 (54% share) | 7.7% | Premium features (unlimited likes); 62% of U.S. revenue. |

| Freemium/In-App Purchases | 2.39 (25% share) | 12.8% | Micro-transactions; Gen Z favorite. |

| Advertising | 1.46 (15% share) | 5.95% | Targeted ads; declining due to privacy regs. |

| Other (À La Carte) | 0.60 (6% share) | 10.6% | Pay-per-match; niche elite services. |

- Insights: Subscriptions ensure recurring revenue (e.g., Match Group’s model), but freemium converts 20% of free users annually.

4. By Geography: Asia’s Ascendancy

Regional variations highlight cultural and tech adoption differences.

| Region | 2025 Revenue (USD Bn) | CAGR (2025-2030) | Key Markets & Drivers |

|---|---|---|---|

| North America | 2.21 (23% share) | 8.07% | U.S. ($1.65 Bn); mature apps (Tinder, Bumble); 30% adult usage. |

| Europe | 2.61 (27% share) | 6.0% | UK/Germany ($1.0–1.2 Bn); privacy-focused (GDPR); 28% share. |

| Asia-Pacific | 3.38 (35% share) | 13.48% | China ($1.23 Bn); India ($0.78 Bn); 240 Mn singles; AI govt. apps. |

| Latin America/MEA | 1.45 (15% share) | 11.0% | Emerging; Brazil/India diaspora; cultural shifts. |

- Insights: APAC’s boom (e.g., Shaadi.com in India) contrasts North America’s saturation; emerging markets offer 2x ARPU growth potential.

Emerging Trends and Opportunities

- AI & Tech Integration: 68% of platforms now use AI for matching; VR dating projected at $1.8 Bn by 2030.

- Niche Explosion: Muslim/LGBTQ+ segments grow 3x faster; sustainability-focused “ethical dating” at 25% CAGR.

- Post-Pandemic Shifts: 40% growth in paid services; hybrid events blend online/offline.

- Challenges: Data privacy (e.g., U.S. FTC rules) and burnout could cap growth at 1.92% overall.

Opportunities lie in underserved niches (e.g., 50+ in APAC) and B2B extensions like corporate matchmaking.

Conclusion: Positioning for 2030 Growth

The matchmaking market’s segments reveal a dynamic landscape where personalization trumps volume. With USD 9.65 billion in play for 2025, stakeholders should prioritize AI-enhanced niches, regional customization, and subscription innovations to ride the 7.83% CAGR wave. As Gen Z redefines “love” via ethics and tech, the winners will be those fostering authentic connections human or algorithmic.

Read our Regional Reports

- https://www.zionmarketresearch.com/de/report/smart-retail-beacons-market

- https://www.zionmarketresearch.com/de/report/nasal-delivery-devices-market

- https://www.zionmarketresearch.com/de/report/long-term-care-insurance-market

- https://www.zionmarketresearch.com/de/report/outsourced-customer-care-services-market

- https://www.zionmarketresearch.com/de/report/trimethylhydroquinone-market

- https://www.zionmarketresearch.com/de/report/sterilization-services-market